The rise of the Perennial Shoppers

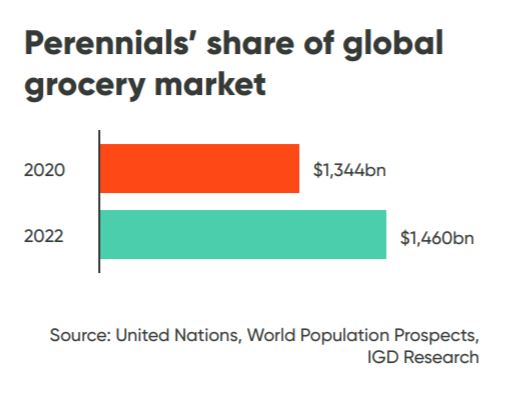

Digitally savvy, experimental and willing to spend more for quality, one significant group of shoppers is set to drive the international grocery sector up by an incremental $116bn over the next couple of years, creating a $1,460bn opportunity by 2022. Accounting for 30% of all food and drink spend across three key markets, new flagship research from IGD shows that this is one age group to invest in for the future. Move over Millennials, it’s time to meet Generation P: The Perennial Shoppers.

Comprising those aged 50-64, Generation P presents a key opportunity for international grocery retail as the group is set to grow in size and significance over the next two years, notably in the UK, Singapore and USA. Across the three markets, IGD’s research has identified opportunities for retailers and suppliers to engage with these shoppers.

Simon Wainwright, Director of Global Insight at IGD, said: “This research shows how significant Perennials are to the global grocery sector. They are an engaged group of shoppers who are accessible when approached in the right way. Competition is already fierce between retailers looking to find new ways to attract shoppers and COVID-19 has made it hard to chart the future. Having a clear focus on your shoppers and knowing how best to reach them will be crucial to success. That’s why the time is right to focus on this often-overlooked group.”

At an international level, Generation P:

Are increasingly engaged in online grocery shoppers. Over half (56%) of Generation P shop online for food sometimes, with a third (33%) predicting they will do more in the future;

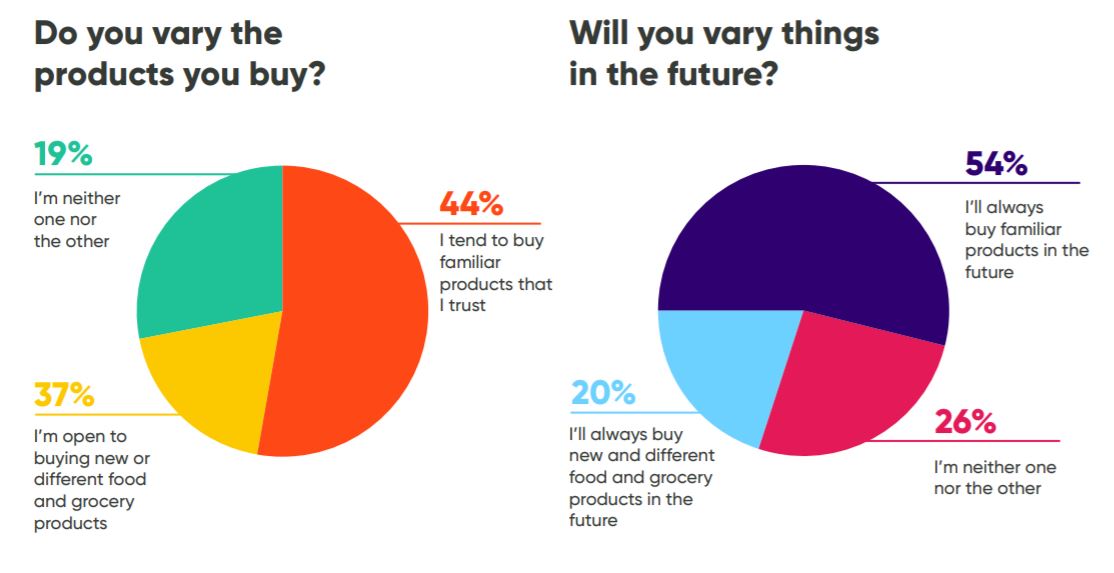

Have an affinity with brands that they have grown up with, but also hold private label products in the same high regard. While 67% of these shoppers buy particular brands because they have grown up with them, the same number (68%) indicate that they are also very satisfied with the quality of own-label products, with 58% trusting them as much as brands;

Value convenience and quality over price. A significant 75% of 50-64-year-olds say they are sometimes tempted to spend more on better quality products, and 56% will sometimes spend more on products because they are easier to prepare and cook;

Would like to select products with specific ethical or environmental credentials but tend to prioritise other factors in their purchasing decisions. Looking into the future, over half of Generation P (54%) indicate that issues around the environment will take on greater importance for them, however, 49% admit they will always prioritise factors such as quality and price.

Regional differences – the UK, Singapore and the USA

Though all united by the fact of being in the same age group and at a closely similar life stage, Perennials of the USA, the UK and Singapore show some clear differences which may be expected to arise from the contrasting social, economic, cultural and even geographical conditions and characteristics found in each country.

UK Perennials are:

The most likely to buy new and different food and grocery products – 42% vs. 34% of Singaporean shoppers and 36% of USA shoppers

The most likely to cook from scratch – 69% vs. 63% of USA shoppers and 58% of Singaporean shoppers

The least likely to buy prepared foods or eat out – 15% vs 23% of USA shoppers and 25% of Singaporean shoppers

The most likely to prioritise specific ethical and environmental factors in their shopping such as animal welfare (61% vs. 50% in the US and 37% in Singapore) and reducing the amount of packaging (53% vs. 39% in the US and 26% in Singapore)

The most likely to check out offers in-store and buy on impulse - 40% vs. 31% in the US and 28% in Singapore

The least likely to plan their shopping trip – 39% vs 55% in the US and 55% in Singapore.

Singapore Perennials are:

More likely to have shopped online for their food and groceries – 72% vs. 55% of UK shoppers and 44% of US shoppers

Most interested in new and relevant technology – 48% vs. 39% of UK shoppers and 46% of US shoppers

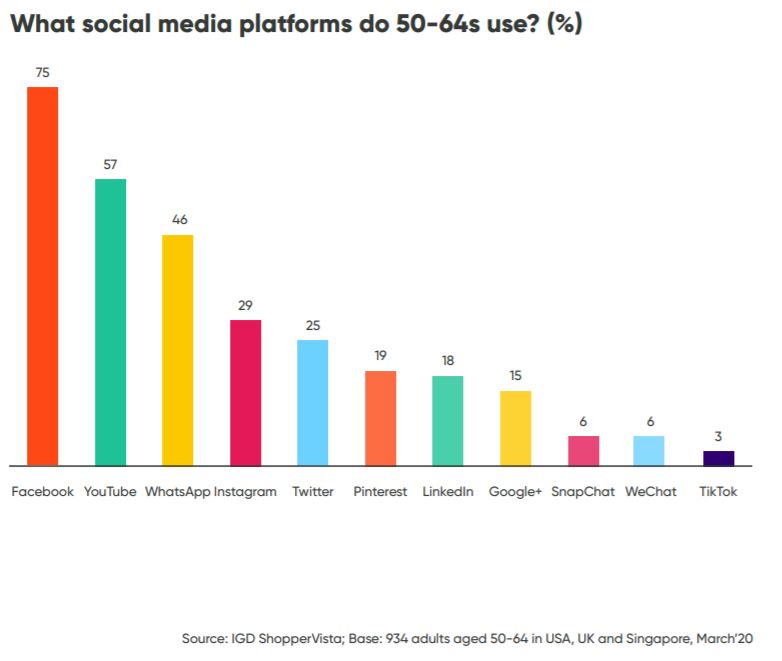

Most engaged with social media – 99% vs. 94% of UK shoppers and 86% of US shoppers

The users of the widest range of social media platforms (including 90% usage of WhatsApp contrasting starkly with 7% in the US where the platform is largely unknown).

US Perennials are:

More likely to buy familiar products than try new things – 49% vs. 32% of UK shoppers

The most confident of identifying good value in food and grocery products – 79% vs 64% of Singaporean shoppers

The most likely to do a big weekly shop (75% vs 57% of Singaporean shoppers) and least likely to shop on a daily basis (17% vs 32% of Singaporean shoppers.

The least likely to shop for food and groceries online with only 44% ever having shopped through the channel.

Commenting on the opportunities with this age group, Simon Wainwright said: “Perennials have embedded digital and online behaviours which they will carry forward and continue to develop into later life. However, this is a generation that doesn’t go digital purely for the sake of going digital – adoption of new technologies for them is driven by their proven practical benefits, and these have to outweigh those of established interactions and processes, such as traditional ‘analogue’ store-based shopping.

“Perennial shoppers show aspects of being habitual both in how they shop and in having an affinity for products that are familiar to them. In cases where they have grown up with products this affinity clearly can go back decades. However, it is clear that they also continue to evolve in terms of their tastes and choices, showing an ongoing willingness to trial new and different products as well as pragmatic considerations such as balancing quality with value for money.”

As families gear up for summer gatherings, APPLEGATE®, the nation’s leading natural and...

The GCC is a trade bloc comprising UAE, Saudi Arabia, Bahrain, Oman, Qatar and Kuwait. AHDB&rsquo...

Less preparation, more barbecue Barbecuing increasingly fits into everyday routines, making spee...